Outline:

- If the price changes, will the demand change?

- If demand of the product changes drastically when its price increases or decreases, it is considered elastic;

- If the quantity demand of the product changes very little when its price fluctuates, it is considered inelastic;

Elasticity is the measure of how one economic variable (demand, supply) responds to a change in another.

Once we understand elasticity we can answer questions such as:

-

If I lower the price of my product, will I sell more? If so, how much more?

-

If I raise the price of my service, how will my sales be affected?

-

If the market price of my product goes down, how will it affect the level of competition in my sector?

Let's focus on price elasticity for now; the measure of how responsive the quantity demanded or supplied of a good is to a change in price.

Generally, you can describe a product as either elastic–very responsive–unit elastic, or inelastic–not very responsive.

-

An elastic demand (or supply) curve shows us the quantity demanded (or supplied) will respond to price changes in a greater proportion than the change in price;

-

An inelastic demand (or supply) curve is the exact opposite. The quantity demanded (or supplied) will respond in a lesser proportion than the change in price; and

-

Unit elasticity means a change in price will lead to the same change in quantity demanded (or supplied).

We measure price elasticity as the percentage change in quantity demanded (or supplied) divided by the percentage change in price. It's a differential calculus problem - we're measuring the responsiveness of one variable to changes in another. The causative variable is, in this case, price.

The good thing about elasticity as a concept is that it is a unitless ratio, meaning it is independent of the type of quantities. This is what allows us to compare a change in price to a change in demand.

Like utility, elasticity is one of the most important concepts of neoclassical economics. It'll help you understand the incidence of indirect taxation, marginal concepts, distribution of wealth, and how consumers pick different goods (the theory of consumer choice).

Price elasticity: supply and demand

Both the supply and demand curves show us the relationship between price and the number of units supplied or demanded. Price elasticity takes this idea one step further, showing us how a percentage change in supply (or demand) corresponds to a percentage change in price.

In simple terms, it shows us how changing the price affects the quantity supplied and the quantity demanded in concrete terms.

-

The price elasticity of supply is the percentage change in quantity supplied of a good or service divided by the percentage change in price; and

-

The price elasticity of demand is the percentage change in the quantity demanded of a good or service divided by the percentage change in price.

Generally, something is elastic if the change in quantity divided by change in price is greater than one, unitary if equals one, and inelastic if less than one. One thing to consider is that the elasticity of a good can change depending on the current quantity demanded/supplied and the price.

Elasticity varies between products

Elasticity can vary between products because some things are more essential than others, or they don't have any good substitutes. Demand for necessities (food, water, housing) tends to be less sensitive to price changes than other goods because consumers will continue to need (and buy) these products despite price increases.

Inversely, goods that are far less necessary (like a Coke) tend to be far more elastic, because the opportunity cost of buying the product becomes too high. The goods that tend to have the highest price elasticity are ones that are readily available and have good alternatives.

A classic example of this is Coke and Pepsi. If the price of Coke rises, people may swap to Pepsi.

This leads us onto the three main factors that can affect the elasticity:

-

Availability of substitutes;

-

Necessity; and

-

Time.

In general, the more good substitutes a good has, the more elastic the demand will be. Inversely, the more necessary a good is for survival the less elastic the demand will be. Time is a little different to both as it's more of a multiplier.

Imagine if coffee went up by $2 at your local coffee shop. You might like the coffee there so there aren't any ‘good’ available substitutes, so you continue to buy coffee despite the increase in price. This would suggest that coffee is inelastic because the change in price hasn't affect the quantity you demand.

However, if you find that you can't afford that additional $2 a day, or you find a new coffee shop you like, the price elasticity of coffee for you may become elastic over the long term.

Extreme cases of elasticity

There are two extreme cases of elasticity:

-

When elasticity equals zero; and

-

When elasticity is infinite.

There is also the unique case of constant unitary elasticity, but let's touch of the two above examples first.

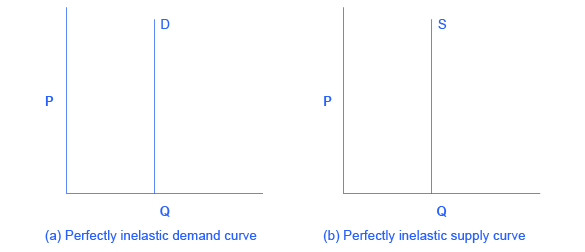

Zero elasticity (or perfect inelasticity) is when a percentage change in price, no matter how large, results in zero change in quantity. The demand and supply curves in this case are vertical.

While this is unlikely, goods that have limited supply often have inelastic supply. Think about Leonardo Da Vinci paintings - no matter how high the price will go, the supply can't change. Inelastic demand is also unlikely, but necessities with no substitutes are likely to have highly inelastic demand. Think about life-saving drugs - people are willing to pay a lot.

Infinite elasticity (or perfect elasticity) is when quantity demanded (or supplied) changes by an infinite amount in response to any change in price. In both cases, the demand (or supply) graph is horizontal.

Again, this isn't realistic, but goods that are easy to produce like books tend to have highly elastic supply curves. Similarly, goods that have readily available substitutes tend to have highly elastic demand curves, a car is a good example.

Closing out

Understanding elasticity is useful because it allows you to understand how pricing affects supply and demand. If you can do that, you can understand how to maximise revenue by either, raising your prices or lowering them.

This plays a key role in any business because it allows you to determine whether increasing costs will add a net benefit (or loss) to the bottom line of the business. The key concept to think about is the price elasticity of demand. If the good you are selling is price inelastic, raise the price.

But keep in mind that just because the quantity demanded hasn't changed in the short term doesn't mean it won't. Remember that time is a factor, and both quantity supplied and quantity demanded are often slow to react to changes in price, but in the long term they tend to.

This is because suppliers tend to find it easier to expand production after they know that the demand will continue. After all, if the demand is short-lived but they've increased supply, they won't be able to sell the additional goods (unless they lower the price to meet demand).